Storage Heartland – Australia can move from Global Testbed to Export Powerhouse

Posted at 27th August, 2020, 13:08:00 in News// by Julie Frikken //

To understand the potential economic impact of leading a large, booming global industry, one need only look to what tech has done for the US. Some argue that tech alone has propped up confidence across all US indices throughout 2020, and it is hard to argue with that.

It can be said that economies can be categorised as skilfully managing either adversity or prosperity. The US does not get everything right, but they know a thing or two about fostering innovation, capitalising on their strengths and helping their home-grown brands to scale globally, often to an incomprehensible level.

Apple’s market capitalisation soared to US $2T last week, greater than the GDP of Australia, Italy, Brazil, Canada, Russia and South Korea, among others. This made it the first US company to reach the milestone.

Apple achieved this in the middle of a global recession, which no one can deny is impressive. But here’s where it gets interesting. Out of the 500 companies included in the S&P 500, considered the US stock market’s performance barometer, only six are responsible for the index being in the black this year. And they are all in tech: Apple, Facebook, Amazon, Netflix and Google’s Alphabet.

While the tech industry may not offer a 100% apples-to-apples comparison, it certainly serves as an example of the economic gains achieved when a country spearheads mass global transformation. And I would challenge anyone to identify a sector more favourably positioned than energy for a market boom today. In fact, when you consider the sheer magnitude of the energy transition taking place, it certainly seems worthy of comparison to the birth of widespread internet in the mid 1990s. This must not be underestimated.

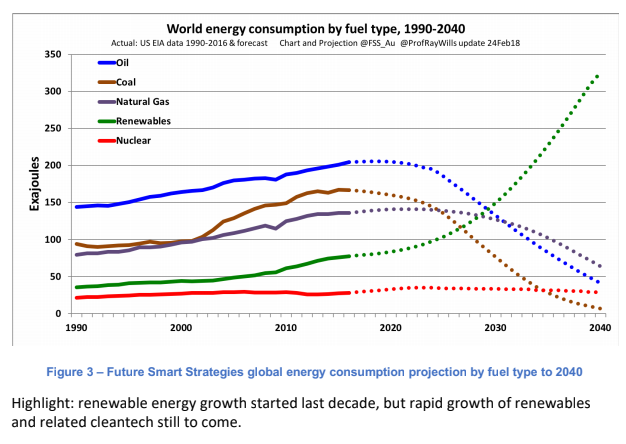

In 2019, Bloomberg New Energy Finance forecasted that renewable energy will account for 50% of global generation by 2050. The International Energy Agency (IEA) projects renewables to expand by 50% in the next five years alone.

This growth is intrinsically linked to battery storage because the renewables hosting capacity of electricity grids relies upon a baseline of dispatchable generation. Batteries are the prime candidate to meet this need whilst adhering to emissions reduction targets. Wood Mackenzie forecasts the battery storage market to grow thirteen-fold by 2024, and Bloomberg New Energy Finance projects the battery industry to be valued at $US620 billion by 2050.

These are very BIG numbers.

Now let’s look at how Australia is positioned.

Australia is already the global epicentre of stationary storage adoption

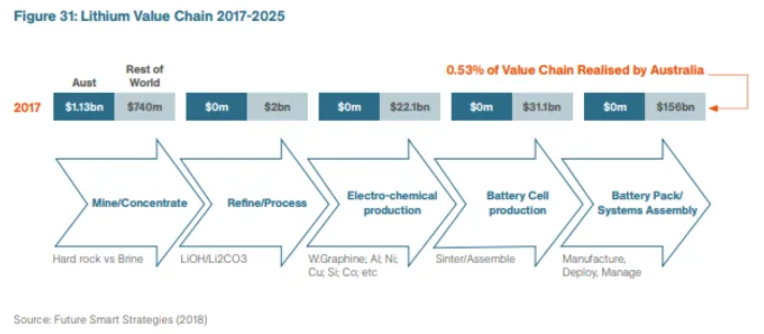

Much has been reported about the incredibly fortunate position Australia has found itself in in battery storage, but as this 2019 article published by the Financial Review explains, our chance to move from just a raw materials producer to a leading processor and manufacturer will not remain open indefinitely.

Globally, Australia has the highest penetration of solar PV and also pays the highest tariffs for electricity. Driven by solar-plus-storage projects, our competitive energy markets and the attractive economics of self-generated solar power, Australia led the world in the global rollout of residential storage in 2018 with 150 megawatts, or 300 megawatt-hours, of systems deployed. Globally, battery manufacturers swarmed the Australian market, ignoring other markets and moving rapidly to set up a local presence here. Very few made the move to manufacture locally, opting to import from cheaper labour markets.

And perhaps the most lucrative piece of the value chain: Australia is sitting on the world’s third largest reserves of lithium, and we are the biggest producer of hard rock lithium spodumene. Coal and gas may be in decline but we have these resources in abundance and it’s time to turn our attention to the future.

Other components of batteries such as precursor, anode, cathode and electrolyte can be manufactured here in Australia, meaning we could capture the entire value chain from raw minerals through to battery manufacturing.

Yet, it was disheartening to read a report from Austrade in December 2018 which showed that Australia captured just 0.5% of the lithium-ion battery value chain, despite being responsible for about 50 per cent of global lithium supply. This meant that about $200 billion worth of processing and manufacturing was completed in foreign markets, mostly using materials exported from Australia, only to be repurchased at a premium.

Image: Processing Plant at Lithium Mine in Western Australia. Mechanical processing used to refine lithium spodumene concentrate

With all the required raw materials, research capability, a thriving local market and the availability of skilled labour, the only missing piece of the value chain here is manufacturing. However, analysis conducted by Energy Renaissance has shown that the delta is far less when comparing the cost of advanced manufacturing.

Australia has everything it takes to build a thriving battery storage industry. So what could federal and state governments do to capitalise on this opportunity?

Improvements in EV uptake

Australia is heavily dependent on foreign oil. Our transport sector accounts for one fifth of national emissions and yet, EVs make up just 0.6% of total vehicle sales.

Meanwhile in Norway, as this RenewEconomy article outlines, one in two car sales are electric, and EVs accounted for 70% of all car purchases in April 2020. This has been achieved through the provision of consistent support across successive governments for many decades, with a suite of EV policies established to streamline the roll out of electric vehicle infrastructure.

Energeia’s Australian EV market study estimates that with no intervention Australia will reach 50 per cent of EVs in the total car fleet around 2045. This could be accelerated by:

Reclassifying EVs to standard vehicles instead of luxury (avoiding an exorbitant tax at point of purchase)

Reducing company car tax on EVs

Waiving stamp duty on EVs

Offering a discount on registration fees

Provide exemptions or discounts on road tolls

Added benefits such as access to bus lanes and free use of ferries as is done in Norway

This alone would result in an immediate spike in EV uptake and stimulate demand for more batteries.

Attracting battery manufacturers

The common theme among countries who are rapidly scaling renewable energy is that their leaders set aggressive targets for renewable generation and this is supported with investments. Having strong targets brings market certainty to ensure large scale projects get funded. In addition, governments could:

Accelerate grid infrastructure projects to accommodate increasing levels of renewable energy and battery storage in areas where it’s needed the most, such as in remote indigenous communities

Subsidise the purchase of batteries until adequate scale is reached in order to make it accessible across socio-economic categories

Provide tax breaks for battery manufacturers

Support for battery manufacturers to employ unskilled labour

Provide education to help communities to establish group buying programs, imbedded networks and community batteries

Subsidies on commercial leases

Ease regulatory hurdles to help fast-track renewable energy and battery storage projects

Invest public funds to augment private investment of renewable energy and battery storage projects

Help to fund critical services such as those provided by the Advanced Manufacturing Growth Centre (AMGC)

Fund programs to educate local manufacturers about exporting to other markets

The Australian economy has ridden on the success of the mining sector for decades, we know how big an impact one sector can have on the national balance sheet, however we’ve never excelled at expanding our place in a global market through vertical integration. The market opportunity presented by renewable energy requires little debate – this is a global revolution at an extraordinary scale.

This topic has been given endless coverage in the media over the past 3 years. We have high demand locally, all the skills, resources and capability to become the global leader in renewables. If Australia does not seize the opportunity right before it – with aggressive action, not passive acceptance – it will go down in history as one of the greatest economic failures of our time.

It is time for Australia to come into its own. Sure, we could sail through passively and yield some benefits, but decades of prosperity await us if we back this industry and claim our share of its explosive, inevitable growth.

Sydney, AUSTRALIA – 6 December 2021 – Construction of our lithium battery gigafactory in Tomago, NSW (Renaissance One) is progressing well, thanks to some sterling wet-weather work from our ...

Sydney, AUSTRALIA – 15 November 2021 – Work on our lithium battery gigafactory in Tomago, NSW (Renaissance One) is picking up pace, with our development partner ATB Morton now erec...

Sydney, AUSTRALIA – 2 November 2021 – The Australian Battery Society, a networking, information and training hub for the battery industry, announced today that it has launched the Energ...